When a vendor flags a transaction as fraudulent or incorrect, a complex system of verification, regulatory compliance, and communication kicks into gear. Efficient dispute workflows are a critical component of both the vendor and buyer experience. Let’s break down the lifecycle of a financial dispute.

The Life of a Dispute

The back-office journey typically follows a structured path. Understanding each stage is key to identifying where bottlenecks occur.

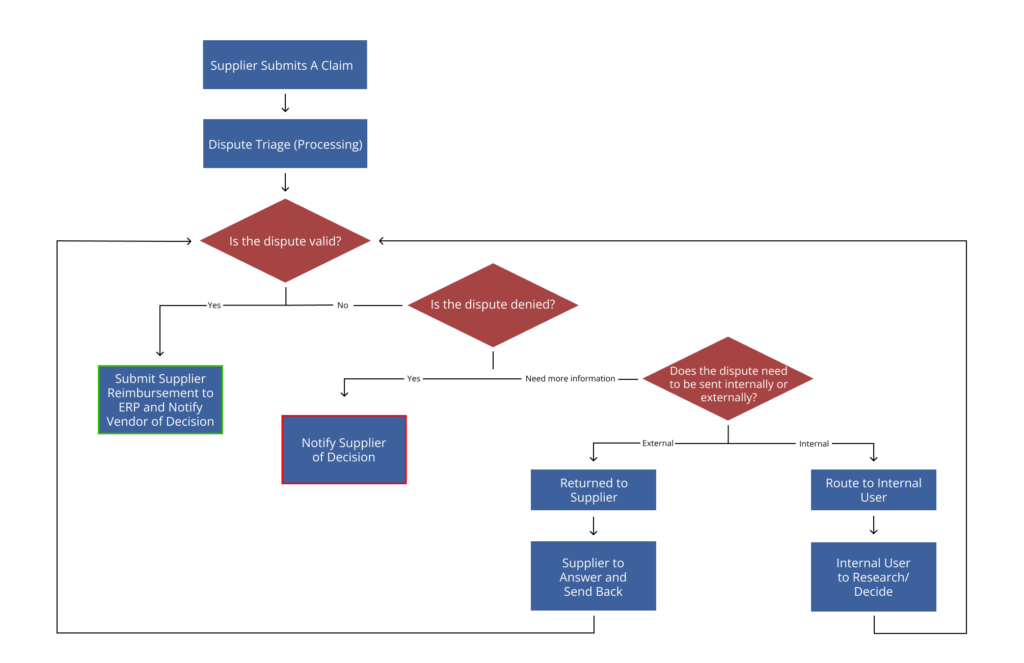

1. Unified Intake & Verification

The process begins the moment a vendor submits a claim.

- The Modern Approach: Instead of disparate forms, modern back offices use unified intake portals. These systems automatically pull transaction data, merchant details, and vendor history into a single case folder.

- Back Office Win: Automated verification checks (like ensuring the dispute is within the 60-day legal window) save hours of manual data entry.

2. Intelligent Categorization

Not all disputes are created equal. Is it a merchant error, a compromise, or a case of establishing an EDI relationship?

- Workflow Integration: Based on the reason code (e.g., “Product Not Received” vs. “Duplicate Charge”), the workflow engine routes the case to the right person. This ensures that high-priority fraud cases are handled by the security team immediately, while simple errors follow a fast-track automated path.

3. The Investigation Phase

This is where data enrichment happens.

- Route Internally or Externally: If there is more information needed about the dispute, it can be automatically routed to internal resources or back to the vendor who must provide more information.

- Automation: AI-driven tools can now summarize responses and highlight discrepancies in a fraction of the time it takes a human to read through pages of PDFs.

Why Manual Workflows Are Failing

Traditionally, the back office relied on spreadsheets and manual emails. This leads to three major pain points:

- Regulatory Risk: Missing a deadline can lead to fines or poor relationships.

- Increased Write-offs: If a resource can’t resolve a small-dollar dispute quickly, it’s often cheaper to “write it off” (pay the customer from the bank’s pocket). Over thousands of cases, this bleeds revenue.

- Vendor Friction: The vendor has no idea what’s happening with their money, which leads to churn.

Self-Service and AI

The video highlights a shift toward more empowered back offices. Implementing a self-service portal allows vendors to track their dispute status in real-time. This reduces “Where is my money?” calls, allowing back-office staff to focus on complex investigations rather than status updates.

Furthermore, integrating AI into the workflow allows for predictive resolution. By analyzing historical data, the system can suggest the most likely outcome of a dispute, helping agents make faster, more accurate decisions.

Final Thoughts

Dispute management is the ultimate “moment of truth” for a bank’s relationship with its customers. By moving away from fragmented, manual processes and toward integrated, AI-enhanced workflows, financial institutions can turn a back-office burden into a competitive advantage.

To see these workflows in action, check out the full breakdown in the original video here.